+

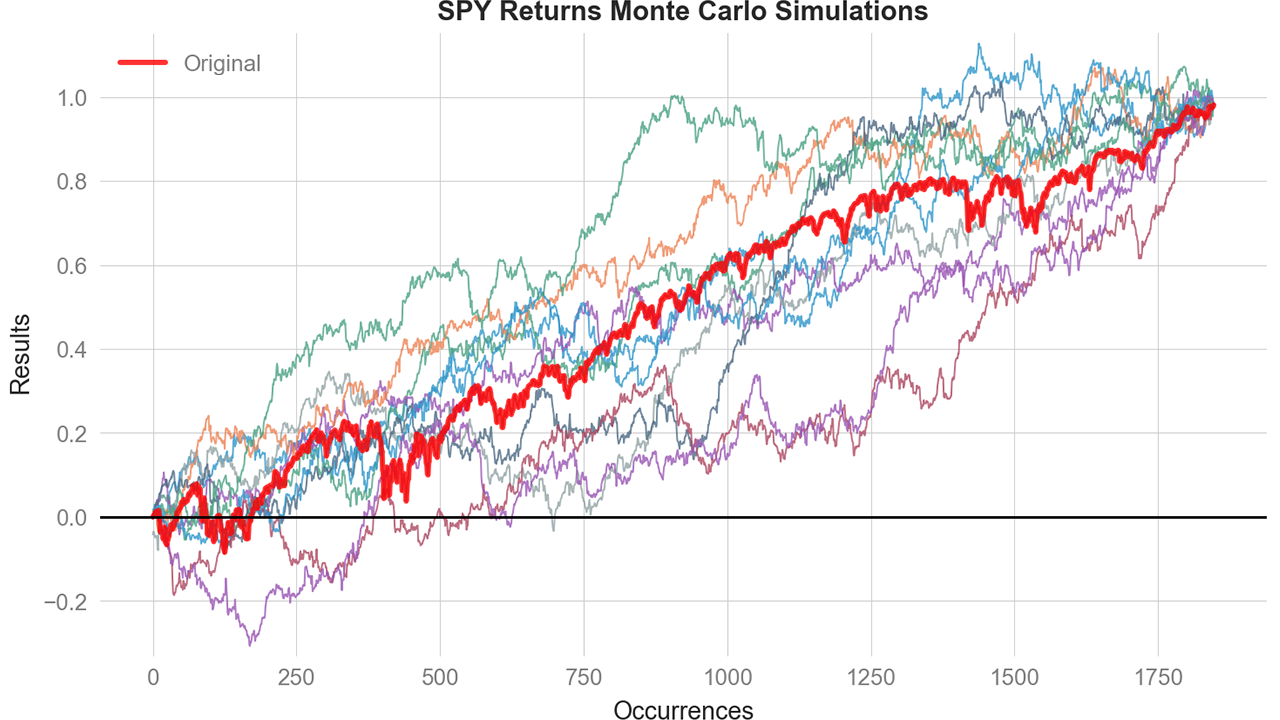

+QuantStats includes built-in [Monte Carlo simulation](https://en.wikipedia.org/wiki/Monte_Carlo_method)

+capabilities for probabilistic risk analysis. Run thousands of simulations by shuffling

+historical returns to understand the range of possible outcomes for your strategy.

+

+## Quick Start

+

+```python

+import quantstats as qs

+

+# fetch daily returns

+returns = qs.utils.download_returns('SPY')

+

+# run Monte Carlo simulation with 1000 paths

+mc = qs.stats.montecarlo(returns, sims=1000, seed=42)

+

+# view terminal value statistics

+print(mc.stats)

+```

+

+Output:

+

+```python

+{

+ 'min': -0.15,

+ 'max': 0.85,

+ 'mean': 0.32,

+ 'median': 0.31,

+ 'std': 0.18,

+ 'percentile_5': 0.05,

+ 'percentile_95': 0.62

+}

+```

+

+## Bust & Goal Probabilities

+

+Calculate the probability of hitting a drawdown threshold (bust) or

+reaching a return goal:

+

+```python

+# Set bust threshold at -20% drawdown, goal at +50% return

+mc = qs.stats.montecarlo(returns, sims=1000, bust=-0.20, goal=0.50, seed=42)

+

+print(f"Probability of bust: {mc.bust_probability:.1%}")

+print(f"Probability of reaching goal: {mc.goal_probability:.1%}")

+```

+

+Output:

+

+```

+Probability of bust: 23.4%

+Probability of reaching goal: 67.8%

+```

+

+## Max Drawdown Distribution

+

+Analyze the distribution of maximum drawdowns across all simulations:

+

+```python

+print(mc.maxdd)

+```

+

+Output:

+

+```python

+{

+ 'min': -0.45, # worst drawdown across all sims

+ 'max': -0.05, # best (smallest) drawdown

+ 'mean': -0.18,

+ 'median': -0.16,

+ 'std': 0.08,

+ 'percentile_5': -0.35,

+ 'percentile_95': -0.08

+}

+```

+

+## Confidence Bands

+

+Get confidence intervals for the simulation paths:

+

+```python

+# 95% confidence band

+lower, upper = mc.confidence_band(0.95)

+

+# specific percentile path

+p10 = mc.percentile(10) # 10th percentile path

+p90 = mc.percentile(90) # 90th percentile path

+```

+

+## Visualization

+

+**Plot all simulation paths:**

+

+```python

+qs.plots.montecarlo(returns, sims=500, seed=42)

+

+# or from an existing result

+mc.plot()

+```

+

+**Plot terminal value distribution:**

+

+```python

+qs.plots.montecarlo_distribution(returns, sims=500, seed=42)

+```

+

+## Pandas Extension

+

+After calling `qs.extend_pandas()`, you can use Monte Carlo directly on Series:

+

+```python

+qs.extend_pandas()

+

+# run simulation directly on a returns Series

+mc = returns.montecarlo(sims=1000, bust=-0.15, goal=0.30)

+

+# plot directly

+returns.plot_montecarlo(sims=500)

+```

+

+## Sharpe, Drawdown & CAGR Distributions

+

+Get distributions of key metrics across simulations:

+

+```python

+# Sharpe ratio distribution

+sharpe_dist = qs.stats.montecarlo_sharpe(returns, sims=1000)

+print(f"Sharpe range: {sharpe_dist['percentile_5']:.2f} to {sharpe_dist['percentile_95']:.2f}")

+

+# Max drawdown distribution

+dd_dist = qs.stats.montecarlo_drawdown(returns, sims=1000)

+print(f"Drawdown range: {dd_dist['percentile_5']:.1%} to {dd_dist['percentile_95']:.1%}")

+

+# CAGR distribution

+cagr_dist = qs.stats.montecarlo_cagr(returns, sims=1000)

+print(f"CAGR range: {cagr_dist['percentile_5']:.1%} to {cagr_dist['percentile_95']:.1%}")

+```

+

+## Access Raw Data

+

+The raw simulation data is available as a DataFrame:

+

+```python

+print(mc.data.head())

+```

+

+```

+ sim_0 sim_1 sim_2 sim_3 sim_4 ...

+0 0.000000 0.017745 -0.002586 -0.005346 -0.042107 ...

+1 0.002647 0.017795 -0.002398 0.004795 -0.034664 ...

+2 0.003351 0.020711 0.002926 0.004868 -0.037902 ...

+3 0.007572 0.029275 0.004323 0.012818 -0.044294 ...

+4 0.010900 0.028764 0.009446 0.026309 -0.049399 ...

+```

+

+## How It Works

+

+Monte Carlo simulation in QuantStats uses **return shuffling**:

+

+1. Take your historical returns

+2. Randomly shuffle the order of returns (preserving the distribution)

+3. Calculate cumulative returns for each shuffled path

+4. Repeat for N simulations

+

+This approach:

+

+- Preserves the exact return distribution of your data

+- Breaks any time-series dependencies (autocorrelation)

+- Shows the range of outcomes if returns occurred in different orders

+- Helps quantify luck vs. skill in your strategy's performance

+

+> **Note:** Because shuffling preserves the product of all (1+r) values, the terminal

+> value is the same across all simulations. What differs is the *path* taken to

+> get there, which affects drawdowns, Sharpe ratios, and other path-dependent metrics.

+

+## API Reference

+

+### `qs.stats.montecarlo(returns, sims=1000, bust=None, goal=None, seed=None)`

+

+Run Monte Carlo simulation on returns.

+

+**Parameters:**

+- `returns`: pd.Series of daily returns

+- `sims`: Number of simulations (default: 1000)

+- `bust`: Drawdown threshold for bust probability (e.g., -0.20)

+- `goal`: Return threshold for goal probability (e.g., 0.50)

+- `seed`: Random seed for reproducibility

+

+**Returns:** `MonteCarloResult` object

+

+### MonteCarloResult properties

+

+| Property | Description |

+|----------|-------------|

+| `data` | DataFrame with all simulation paths |

+| `original` | Series with original cumulative returns |

+| `stats` | Dict with terminal value statistics |

+| `maxdd` | Dict with max drawdown statistics |

+| `bust_probability` | Float (if bust threshold set) |

+| `goal_probability` | Float (if goal threshold set) |

+

+### MonteCarloResult methods

+

+| Method | Description |

+|--------|-------------|

+| `percentile(p)` | Get p-th percentile path |

+| `confidence_band(level)` | Get (lower, upper) confidence bounds |

+| `plot(**kwargs)` | Plot simulation paths |

diff --git a/docs/report.jpg b/docs/report.jpg

deleted file mode 100644

index 44841f35..00000000

Binary files a/docs/report.jpg and /dev/null differ

diff --git a/docs/report.webp b/docs/report.webp

new file mode 100644

index 00000000..978d90b7

Binary files /dev/null and b/docs/report.webp differ

diff --git a/docs/snapshot.jpg b/docs/snapshot.jpg

deleted file mode 100644

index 0dcccb71..00000000

Binary files a/docs/snapshot.jpg and /dev/null differ

diff --git a/docs/snapshot.webp b/docs/snapshot.webp

new file mode 100644

index 00000000..d033e685

Binary files /dev/null and b/docs/snapshot.webp differ

diff --git a/docs/tearsheet.html b/docs/tearsheet.html

index 702f80cb..579fcec5 100644

--- a/docs/tearsheet.html

+++ b/docs/tearsheet.html

@@ -1 +1 @@

-

+

+QuantStats includes built-in [Monte Carlo simulation](https://en.wikipedia.org/wiki/Monte_Carlo_method)

+capabilities for probabilistic risk analysis. Run thousands of simulations by shuffling

+historical returns to understand the range of possible outcomes for your strategy.

+

+## Quick Start

+

+```python

+import quantstats as qs

+

+# fetch daily returns

+returns = qs.utils.download_returns('SPY')

+

+# run Monte Carlo simulation with 1000 paths

+mc = qs.stats.montecarlo(returns, sims=1000, seed=42)

+

+# view terminal value statistics

+print(mc.stats)

+```

+

+Output:

+

+```python

+{

+ 'min': -0.15,

+ 'max': 0.85,

+ 'mean': 0.32,

+ 'median': 0.31,

+ 'std': 0.18,

+ 'percentile_5': 0.05,

+ 'percentile_95': 0.62

+}

+```

+

+## Bust & Goal Probabilities

+

+Calculate the probability of hitting a drawdown threshold (bust) or

+reaching a return goal:

+

+```python

+# Set bust threshold at -20% drawdown, goal at +50% return

+mc = qs.stats.montecarlo(returns, sims=1000, bust=-0.20, goal=0.50, seed=42)

+

+print(f"Probability of bust: {mc.bust_probability:.1%}")

+print(f"Probability of reaching goal: {mc.goal_probability:.1%}")

+```

+

+Output:

+

+```

+Probability of bust: 23.4%

+Probability of reaching goal: 67.8%

+```

+

+## Max Drawdown Distribution

+

+Analyze the distribution of maximum drawdowns across all simulations:

+

+```python

+print(mc.maxdd)

+```

+

+Output:

+

+```python

+{

+ 'min': -0.45, # worst drawdown across all sims

+ 'max': -0.05, # best (smallest) drawdown

+ 'mean': -0.18,

+ 'median': -0.16,

+ 'std': 0.08,

+ 'percentile_5': -0.35,

+ 'percentile_95': -0.08

+}

+```

+

+## Confidence Bands

+

+Get confidence intervals for the simulation paths:

+

+```python

+# 95% confidence band

+lower, upper = mc.confidence_band(0.95)

+

+# specific percentile path

+p10 = mc.percentile(10) # 10th percentile path

+p90 = mc.percentile(90) # 90th percentile path

+```

+

+## Visualization

+

+**Plot all simulation paths:**

+

+```python

+qs.plots.montecarlo(returns, sims=500, seed=42)

+

+# or from an existing result

+mc.plot()

+```

+

+**Plot terminal value distribution:**

+

+```python

+qs.plots.montecarlo_distribution(returns, sims=500, seed=42)

+```

+

+## Pandas Extension

+

+After calling `qs.extend_pandas()`, you can use Monte Carlo directly on Series:

+

+```python

+qs.extend_pandas()

+

+# run simulation directly on a returns Series

+mc = returns.montecarlo(sims=1000, bust=-0.15, goal=0.30)

+

+# plot directly

+returns.plot_montecarlo(sims=500)

+```

+

+## Sharpe, Drawdown & CAGR Distributions

+

+Get distributions of key metrics across simulations:

+

+```python

+# Sharpe ratio distribution

+sharpe_dist = qs.stats.montecarlo_sharpe(returns, sims=1000)

+print(f"Sharpe range: {sharpe_dist['percentile_5']:.2f} to {sharpe_dist['percentile_95']:.2f}")

+

+# Max drawdown distribution

+dd_dist = qs.stats.montecarlo_drawdown(returns, sims=1000)

+print(f"Drawdown range: {dd_dist['percentile_5']:.1%} to {dd_dist['percentile_95']:.1%}")

+

+# CAGR distribution

+cagr_dist = qs.stats.montecarlo_cagr(returns, sims=1000)

+print(f"CAGR range: {cagr_dist['percentile_5']:.1%} to {cagr_dist['percentile_95']:.1%}")

+```

+

+## Access Raw Data

+

+The raw simulation data is available as a DataFrame:

+

+```python

+print(mc.data.head())

+```

+

+```

+ sim_0 sim_1 sim_2 sim_3 sim_4 ...

+0 0.000000 0.017745 -0.002586 -0.005346 -0.042107 ...

+1 0.002647 0.017795 -0.002398 0.004795 -0.034664 ...

+2 0.003351 0.020711 0.002926 0.004868 -0.037902 ...

+3 0.007572 0.029275 0.004323 0.012818 -0.044294 ...

+4 0.010900 0.028764 0.009446 0.026309 -0.049399 ...

+```

+

+## How It Works

+

+Monte Carlo simulation in QuantStats uses **return shuffling**:

+

+1. Take your historical returns

+2. Randomly shuffle the order of returns (preserving the distribution)

+3. Calculate cumulative returns for each shuffled path

+4. Repeat for N simulations

+

+This approach:

+

+- Preserves the exact return distribution of your data

+- Breaks any time-series dependencies (autocorrelation)

+- Shows the range of outcomes if returns occurred in different orders

+- Helps quantify luck vs. skill in your strategy's performance

+

+> **Note:** Because shuffling preserves the product of all (1+r) values, the terminal

+> value is the same across all simulations. What differs is the *path* taken to

+> get there, which affects drawdowns, Sharpe ratios, and other path-dependent metrics.

+

+## API Reference

+

+### `qs.stats.montecarlo(returns, sims=1000, bust=None, goal=None, seed=None)`

+

+Run Monte Carlo simulation on returns.

+

+**Parameters:**

+- `returns`: pd.Series of daily returns

+- `sims`: Number of simulations (default: 1000)

+- `bust`: Drawdown threshold for bust probability (e.g., -0.20)

+- `goal`: Return threshold for goal probability (e.g., 0.50)

+- `seed`: Random seed for reproducibility

+

+**Returns:** `MonteCarloResult` object

+

+### MonteCarloResult properties

+

+| Property | Description |

+|----------|-------------|

+| `data` | DataFrame with all simulation paths |

+| `original` | Series with original cumulative returns |

+| `stats` | Dict with terminal value statistics |

+| `maxdd` | Dict with max drawdown statistics |

+| `bust_probability` | Float (if bust threshold set) |

+| `goal_probability` | Float (if goal threshold set) |

+

+### MonteCarloResult methods

+

+| Method | Description |

+|--------|-------------|

+| `percentile(p)` | Get p-th percentile path |

+| `confidence_band(level)` | Get (lower, upper) confidence bounds |

+| `plot(**kwargs)` | Plot simulation paths |

diff --git a/docs/report.jpg b/docs/report.jpg

deleted file mode 100644

index 44841f35..00000000

Binary files a/docs/report.jpg and /dev/null differ

diff --git a/docs/report.webp b/docs/report.webp

new file mode 100644

index 00000000..978d90b7

Binary files /dev/null and b/docs/report.webp differ

diff --git a/docs/snapshot.jpg b/docs/snapshot.jpg

deleted file mode 100644

index 0dcccb71..00000000

Binary files a/docs/snapshot.jpg and /dev/null differ

diff --git a/docs/snapshot.webp b/docs/snapshot.webp

new file mode 100644

index 00000000..d033e685

Binary files /dev/null and b/docs/snapshot.webp differ

diff --git a/docs/tearsheet.html b/docs/tearsheet.html

index 702f80cb..579fcec5 100644

--- a/docs/tearsheet.html

+++ b/docs/tearsheet.html

@@ -1 +1 @@

- Facebook Buy & Hold "Strategy" 18 May, 2012 - 7 May, 2019

Generated by QuantStats for Python (v. 0.0.01)

Key Performance Metrics

| Metric | Strategy | Benchmark |

|---|---|---|

| Risk-free rate | 0.0% | 0.0% |

| Exposure % | 100.0% | 100.0% |

| Total Return | 402.17% | 155.79% |

| CAGR% | 22.16% | 6.58% |

| Sharpe | 0.81 | 1.11 |

| Sortino | 1.15 | 1.43 |

| Max Drawdown | -36.54% | -13.89% |

| Longest DD Days | 441 | 272 |

| Volatility (ann.) | 37.02% | 12.89% |

| R^2 | 0.15 | 0.15 |

| Calmar | 0.41 | 0.34 |

| Skew | 1.31 | -0.36 |

| Kurtosis | 22.95 | 3.52 |

| Expected Daily % | 0.09% | 0.05% |

| Expected Monthly % | 1.92% | 1.11% |

| Expected Yearly % | 22.35% | 12.46% |

| Kelly Criterion | 93.06% | 91.98% |

| Risk of Ruin | 0.0% | 0.0% |

| Daily Value-at-Risk | 5.54% | 1.95% |

| Expected Shortfall (cVaR) | 6.33% | 2.22% |

| Payoff Ratio | -1.17 | -1.22 |

| Profit Factor | 0.17 | 0.22 |

| Common Sense Ratio | 0.19 | 0.21 |

| CPC Index | -0.11 | -0.15 |

| Tail Ratio | 1.11 | 0.96 |

| Outlier Win Ratio | 2.64 | 7.26 |

| Outlier Loss Ratio | 2.82 | 7.08 |

| MTD | -0.73% | -1.13% |

| 3M | 13.43% | 7.36% |

| 6M | 29.12% | 7.43% |

| YTD | 46.45% | 16.84% |

| 1Y | 8.7% | 11.4% |

| 3Y (ann.) | -15.38% | -20.77% |

| 5Y (ann.) | 17.94% | -6.4% |

| 10Y (ann.) | 22.16% | 6.58% |

| All-time (ann.) | 22.16% | 6.58% |

| Best Day | 29.61% | 5.05% |

| Worst Day | -18.96% | -4.18% |

| Best Month | 47.91% | 8.53% |

| Worst Month | -30.19% | -8.81% |

| Best Year | 105.3% | 32.3% |

| Worst Year | -30.37% | -4.57% |

| Avg. Drawdown | -3.35% | -0.85% |

| Avg. Drawdown Days | 26 | 15 |

| Recovery Factor | 7.5 | 8.05 |

| Avg. Up Month | 5.14% | 1.86% |

| Avg. Down Month | -2.66% | -0.7% |

| Win Days % | 52.64% | 55.84% |

| Win Month % | 61.18% | 75.29% |

| Win Quarter % | 68.97% | 86.21% |

| Win Year % | 75.0% | 87.5% |

| Beta | 1.11 | - |

| Alpha | 0.14 | - |

EOY Returns vs Benchmark

| Year | Benchmark | Strategy | Diff% | Won |

|---|---|---|---|---|

| 2012 | 10.75 | -30.37 | -2.82 | - |

| 2013 | 32.30 | 105.30 | 3.26 | + |

| 2014 | 13.46 | 42.76 | 3.18 | + |

| 2015 | 1.24 | 34.15 | 27.57 | + |

| 2016 | 12.00 | 9.93 | 0.83 | - |

| 2017 | 21.70 | 53.38 | 2.46 | + |

| 2018 | -4.57 | -25.71 | 5.62 | - |

| 2019 | 16.84 | 46.45 | 2.76 | + |

Worst 10 Drawdowns

| Started | Recovered | Drawdown | Days |

|---|---|---|---|

| 2018-07-26 | 2019-05-07 | -36.54 | 285 |

| 2012-05-21 | 2013-08-05 | -26.81 | 441 |

| 2018-02-02 | 2018-06-01 | -17.67 | 119 |

| 2014-03-11 | 2014-07-24 | -14.41 | 135 |

| 2015-07-22 | 2015-10-19 | -11.93 | 89 |

| 2016-10-25 | 2017-02-08 | -10.63 | 106 |

| 2013-10-21 | 2013-12-17 | -10.17 | 57 |

| 2016-02-02 | 2016-03-29 | -10.14 | 56 |

| 2015-11-12 | 2016-01-28 | -10.09 | 77 |

| 2016-05-11 | 2016-07-19 | -7.26 | 69 |

Strategy Tearsheet 15 Jul, 2015 - 11 Jul, 2025

Benchmark is SPY | Generated by QuantStats (v. 0.0.64)

Key Performance Metrics

| Metric | SPY | Strategy |

|---|---|---|

| Risk-Free Rate | 0.0% | 0.0% |

| Time in Market | 100.0% | 100.0% |

| Cumulative Return | 251.14% | 704.47% |

| CAGR﹪ | 9.06% | 15.49% |

| Sharpe | 0.78 | 0.74 |

| Prob. Sharpe Ratio | 99.26% | 98.95% |

| Smart Sharpe | 0.75 | 0.71 |

| Sortino | 1.1 | 1.07 |

| Smart Sortino | 1.06 | 1.03 |

| Sortino/√2 | 0.78 | 0.75 |

| Smart Sortino/√2 | 0.75 | 0.73 |

| Omega | 1.15 | 1.15 |

| Max Drawdown | -33.72% | -76.74% |

| Max DD Date | 2020-03-23 | 2022-11-03 |

| Max DD Period Start | 2020-02-20 | 2021-09-08 |

| Max DD Period End | 2020-08-07 | 2024-01-18 |

| Longest DD Days | 708 | 863 |

| Volatility (ann.) | 18.3% | 38.4% |

| R^2 | 0.39 | 0.39 |

| Information Ratio | 0.03 | 0.03 |

| Calmar | 0.27 | 0.2 |

| Skew | -0.31 | -0.26 |

| Kurtosis | 13.84 | 20.38 |

| Expected Daily | 0.05% | 0.08% |

| Expected Monthly | 1.04% | 1.74% |

| Expected Yearly | 12.1% | 20.87% |

| Kelly Criterion | 5.62% | 3.1% |

| Risk of Ruin | 0.0% | 0.0% |

| Daily Value-at-Risk | -1.84% | -3.87% |

| Expected Shortfall (cVaR) | -1.84% | -3.87% |

| Max Consecutive Wins | 11 | 20 |

| Max Consecutive Losses | 8 | 7 |

| Gain/Pain Ratio | 0.16 | 0.15 |

| Gain/Pain (1M) | 0.97 | 0.91 |

| Payoff Ratio | 0.91 | 0.95 |

| Profit Factor | 1.16 | 1.15 |

| Common Sense Ratio | 1.08 | 1.09 |

| CPC Index | 0.58 | 0.58 |

| Tail Ratio | 0.93 | 0.95 |

| Outlier Win Ratio | 6.26 | 2.88 |

| Outlier Loss Ratio | 6.12 | 3.05 |

| MTD | 0.93% | -2.79% |

| 3M | 19.23% | 31.44% |

| 6M | 8.07% | 16.7% |

| YTD | 7.04% | 22.75% |

| 1Y | 12.48% | 34.65% |

| 3Y (ann.) | 10.91% | 39.19% |

| 5Y (ann.) | 10.19% | 15.22% |

| 10Y (ann.) | 9.06% | 15.49% |

| All-time (ann.) | 9.06% | 15.49% |

| Best Day | 10.5% | 23.28% |

| Worst Day | -10.94% | -26.39% |

| Best Month | 12.7% | 27.16% |

| Worst Month | -12.49% | -32.63% |

| Best Year | 31.22% | 194.13% |

| Worst Year | -18.18% | -64.22% |

| Avg. Drawdown | -1.69% | -5.51% |

| Avg. Drawdown Days | 18 | 34 |

| Recovery Factor | 4.22 | 3.69 |

| Ulcer Index | 0.07 | 0.23 |

| Serenity Index | 1.61 | 0.66 |

| Avg. Up Month | 3.68% | 8.95% |

| Avg. Down Month | -4.6% | -8.86% |

| Win Days | 55.13% | 52.91% |

| Win Month | 68.6% | 61.98% |

| Win Quarter | 78.05% | 65.85% |

| Win Year | 72.73% | 81.82% |

| Beta | - | 1.3 |

| Alpha | - | 0.1 |

| Correlation | - | 62.11% |

| Treynor Ratio | - | 540.48% |

EOY Returns vs Benchmark

| Year | SPY | Strategy | Multiplier | Won |

|---|---|---|---|---|

| 2015 | -2.15 | 16.70 | -7.77 | + |

| 2016 | 12.00 | 9.93 | 0.83 | - |

| 2017 | 21.71 | 53.38 | 2.46 | + |

| 2018 | -4.57 | -25.71 | 5.63 | - |

| 2019 | 31.22 | 56.57 | 1.81 | + |

| 2020 | 18.33 | 33.09 | 1.80 | + |

| 2021 | 28.73 | 23.13 | 0.81 | - |

| 2022 | -18.18 | -64.22 | 3.53 | - |

| 2023 | 26.18 | 194.13 | 7.42 | + |

| 2024 | 24.89 | 66.05 | 2.65 | + |

| 2025 | 7.04 | 22.75 | 3.23 | + |

Worst 10 Drawdowns

| Started | Recovered | Drawdown | Days |

|---|---|---|---|

| 2021-09-08 | 2024-01-18 | -76.74 | 863 |

| 2018-07-26 | 2020-01-08 | -42.96 | 532 |

| 2020-01-30 | 2020-05-19 | -34.59 | 111 |

| 2025-02-18 | 2025-06-27 | -34.15 | 130 |

| 2018-02-02 | 2018-05-31 | -21.17 | 119 |

| 2020-08-27 | 2021-04-01 | -19.17 | 218 |

| 2024-04-08 | 2024-07-03 | -18.43 | 87 |

| 2015-07-22 | 2015-10-16 | -16.57 | 87 |

| 2024-07-08 | 2024-09-18 | -16.02 | 73 |

| 2016-10-25 | 2017-02-07 | -13.68 | 106 |

- {{title}}

- {{title}}

+

{{title}} {{date_range}}

- Generated by QuantStats (v. {{v}})

+{{title}} {{date_range}}{{matched_dates}}

+ {{params}} Generated by QuantStats (v. {{v}})

diff --git a/quantstats/reports.py b/quantstats/reports.py

index 49345303..315411db 100644

--- a/quantstats/reports.py

+++ b/quantstats/reports.py

@@ -1,10 +1,9 @@

#!/usr/bin/env python

-# -*- coding: UTF-8 -*-

#

# QuantStats: Portfolio analytics for quants

# https://github.com/ranaroussi/quantstats

#

-# Copyright 2019 Ran Aroussi

+# Copyright 2019-2025 Ran Aroussi

#

# Licensed under the Apache License, Version 2.0 (the "License");

# you may not use this file except in compliance with the License.

@@ -20,615 +19,2499 @@

import pandas as _pd

import numpy as _np

-from datetime import (

- datetime as _dt, timedelta as _td

-)

+from math import sqrt as _sqrt, ceil as _ceil

+from datetime import datetime as _dt

+from base64 import b64encode as _b64encode

import re as _regex

from tabulate import tabulate as _tabulate

-from . import (

- __version__, stats as _stats,

- utils as _utils, plots as _plots

-)

+from . import __version__

+

+# Lazy imports to avoid circular dependency during package initialization

+_stats = None

+_utils = None

+_plots = None

+

+

+def _get_stats():

+ global _stats

+ if _stats is None:

+ from . import stats

+ _stats = stats

+ return _stats

+

+

+def _get_utils():

+ global _utils

+ if _utils is None:

+ from . import utils

+ _utils = utils

+ return _utils

+

+

+def _get_plots():

+ global _plots

+ if _plots is None:

+ from . import plots

+ _plots = plots

+ return _plots

+from dateutil.relativedelta import relativedelta

+from io import StringIO

+from pathlib import Path

+import tempfile

+import webbrowser

try:

- from IPython.core.display import (

- display as iDisplay, HTML as iHTML

- )

+ from IPython.display import display as iDisplay, HTML as iHTML

except ImportError:

- pass

+ pass # IPython not available, display functions won't be used

+

+

+def _get_trading_periods(periods_per_year=252):

+ """

+ Calculate trading periods for different time windows.

+

+ This helper function computes the number of trading periods for full year

+ and half year periods, which are commonly used in financial calculations

+ for annualization and rolling window analysis.

+

+ Parameters

+ ----------

+ periods_per_year : int, default 252

+ Number of trading periods in a year (e.g., 252 for daily data,

+ 12 for monthly data)

+

+ Returns

+ -------

+ tuple

+ A tuple containing (periods_per_year, half_year_periods)

+

+ Examples

+ --------

+ >>> _get_trading_periods(252) # Daily data

+ (252, 126)

+ >>> _get_trading_periods(12) # Monthly data

+ (12, 6)

+ """

+ # Calculate half year periods using ceiling to ensure we get at least half

+ half_year = _ceil(periods_per_year / 2)

+ return periods_per_year, half_year

+

+

+def _print_parameters_table(

+ benchmark_title=None,

+ periods_per_year=252,

+ rf=0.0,

+ compounded=True,

+ match_dates=True,

+):

+ """

+ Print a formatted parameters table for terminal/console output.

+

+ Parameters

+ ----------

+ benchmark_title : str or None

+ Benchmark name/ticker

+ periods_per_year : int

+ Number of trading periods per year

+ rf : float

+ Risk-free rate

+ compounded : bool

+ Whether returns are compounded

+ match_dates : bool

+ Whether dates are matched with benchmark

+ """

+ width = 40

+ print("=" * width)

+ print(" Parameters")

+ print("-" * width)

+ if benchmark_title:

+ print(f"{'Benchmark':<25}{benchmark_title.upper():>15}")

+ print(f"{'Periods/Year':<25}{periods_per_year:>15}")

+ print(f"{'Risk-Free Rate':<25}{rf:>14.1%}")

+ print(f"{'Compounded':<25}{'Yes' if compounded else 'No':>15}")

+ if benchmark_title:

+ print(f"{'Match Dates':<25}{'Yes' if match_dates else 'No':>15}")

+ print("=" * width)

+ print()

+

+

+def _match_dates(returns, benchmark):

+ """

+ Align returns and benchmark data to start from the same date.

+

+ This function ensures that both the returns and benchmark series start

+ from the same date by finding the latest start date where both series

+ have non-zero values. This is crucial for accurate performance comparisons.

+

+ Parameters

+ ----------

+ returns : pd.Series or pd.DataFrame

+ Returns data that may be a Series or DataFrame with multiple columns

+ benchmark : pd.Series

+ Benchmark returns data

+

+ Returns

+ -------

+ tuple

+ A tuple containing (aligned_returns, aligned_benchmark) both starting

+ from the same date

+

+ Examples

+ --------

+ >>> returns_aligned, bench_aligned = _match_dates(returns, benchmark)

+ """

+ # Handle different types of returns data (Series vs DataFrame)

+ if isinstance(returns, _pd.DataFrame):

+ # For DataFrame, use the first column to find the start date

+ loc = max(returns[returns.columns[0]].ne(0).idxmax(), benchmark.ne(0).idxmax())

+ else:

+ # For Series, find the maximum of start dates for both series

+ loc = max(returns.ne(0).idxmax(), benchmark.ne(0).idxmax())

+

+ # Slice both series to start from the latest common start date

+ returns = returns.loc[loc:]

+ benchmark = benchmark.loc[loc:]

+

+ return returns, benchmark

+

+

+def html(

+ returns,

+ benchmark=None,

+ rf=0.0,

+ grayscale=False,

+ title="Strategy Tearsheet",

+ output=None,

+ compounded=True,

+ periods_per_year=252,

+ download_filename="quantstats-tearsheet.html",

+ figfmt="svg",

+ template_path=None,

+ match_dates=True,

+ **kwargs,

+):

+ """

+ Generate an HTML tearsheet report for portfolio performance analysis.

+

+ This function creates a comprehensive HTML report containing performance

+ metrics, visualizations, and analysis of investment returns. The report

+ includes comparisons with benchmarks, drawdown analysis, and various

+ performance charts.

+

+ Parameters

+ ----------

+ returns : pd.Series or pd.DataFrame

+ Daily returns data for the strategy/portfolio

+ benchmark : pd.Series, str, or None, default None

+ Benchmark returns for comparison. Can be a Series of returns,

+ a ticker symbol string, or None for no benchmark

+ rf : float, default 0.0

+ Risk-free rate for calculations (as decimal, e.g., 0.02 for 2%)

+ grayscale : bool, default False

+ Whether to generate charts in grayscale instead of color

+ title : str, default "Strategy Tearsheet"

+ Title to display at the top of the HTML report

+ output : str or None, default None

+ File path to save the HTML report. If None, downloads in browser

+ compounded : bool, default True

+ Whether to compound returns for calculations

+ periods_per_year : int, default 252

+ Number of trading periods per year for annualization

+ download_filename : str, default "quantstats-tearsheet.html"

+ Filename for browser download if output is None

+ figfmt : str, default "svg"

+ Format for embedded charts ('svg', 'png', 'jpg')

+ template_path : str or None, default None

+ Path to custom HTML template file. Uses default if None

+ match_dates : bool, default True

+ Whether to align returns and benchmark start dates

+ **kwargs

+ Additional keyword arguments for customization:

+ - strategy_title: Custom name for the strategy

+ - benchmark_title: Custom name for the benchmark

+ - active_returns: Whether to show active returns vs benchmark

+

+ Returns

+ -------

+ None

+ Generates HTML file either as download or saved to specified path

+

+ Examples

+ --------

+ >>> html(returns, benchmark='^GSPC', title='My Strategy')

+ >>> html(returns, output='report.html', grayscale=True)

+

+ Raises

+ ------

+ FileNotFoundError

+ If custom template_path doesn't exist

+ """

+ # Clean returns data by removing NaN values if date matching is enabled

+ if match_dates:

+ returns = returns.dropna()

+

+ # Get trading periods for calculations

+ win_year, win_half_year = _get_trading_periods(periods_per_year)

+

+ # Secure file path handling for HTML template

+ if template_path is None:

+ # Use default template path - report.html in same directory

+ template_path = Path(__file__).parent / 'report.html'

+ else:

+ template_path = Path(template_path)

+ # Resolve to absolute path and validate template file existence

+ template_path = template_path.resolve()

-def html(returns, benchmark=None, rf=0.,

- grayscale=False, title='Strategy Tearsheet',

- output=None, compounded=True):

+ if not template_path.exists():

+ raise FileNotFoundError(f"Template file not found: {template_path}")

+ if not template_path.is_file():

+ raise ValueError(f"Template path is not a file: {template_path}")

- if output is None and not _utils._in_notebook():

- raise ValueError("`file` must be specified")

+ # Read template securely with UTF-8 encoding

+ tpl = template_path.read_text(encoding='utf-8')

- tpl = ""

- with open(__file__[:-4] + '.html') as f:

- tpl = f.read()

- f.close()

+ # prepare timeseries

+ if match_dates:

+ returns = returns.dropna()

+ # Clean and prepare returns data for analysis

+ returns = _get_utils()._prepare_returns(returns)

- date_range = returns.index.strftime('%e %b, %Y')

- tpl = tpl.replace('{{date_range}}', date_range[0] + ' - ' + date_range[-1])

- tpl = tpl.replace('{{title}}', title)

- tpl = tpl.replace('{{v}}', __version__)

+ # Handle strategy title - can be single string or list for multiple columns

+ strategy_title = kwargs.get("strategy_title", "Strategy")

+ if isinstance(returns, _pd.DataFrame):

+ if len(returns.columns) > 1 and isinstance(strategy_title, str):

+ strategy_title = list(returns.columns)

- mtrx = metrics(returns=returns, benchmark=benchmark,

- rf=rf, display=False, mode='full',

- sep=True, internal="True",

- compounded=compounded)[2:]

- mtrx.index.name = 'Metric'

- tpl = tpl.replace('{{metrics}}', _html_table(mtrx))

- tpl = tpl.replace('

{str_td} ", '

" + StringIO(html_str).read() + ) + tpl = tpl.replace("{{dd_info}}", dd_html_table) + + # Get active returns setting for plots + active = kwargs.get("active_returns", False) + + # Generate all the performance plots and embed them in the HTML # plots - figfile = _utils._file_stream() - _plots.returns(returns, benchmark, grayscale=grayscale, - figsize=(8, 5), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, cumulative=compounded) - tpl = tpl.replace('{{returns}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.log_returns(returns, benchmark, grayscale=grayscale, - figsize=(8, 4), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, cumulative=compounded) - tpl = tpl.replace('{{log_returns}}', figfile.getvalue().decode()) + figfile = _get_utils()._file_stream() + _get_plots().returns( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 5), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compound=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{returns}}", _embed_figure(figfile, figfmt)) + + # Log returns plot for better visualization of performance + figfile = _get_utils()._file_stream() + _get_plots().log_returns( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compound=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{log_returns}}", _embed_figure(figfile, figfmt)) + # Volatility-matched returns plot (only if benchmark exists) if benchmark is not None: - figfile = _utils._file_stream() - _plots.returns(returns, benchmark, match_volatility=True, - grayscale=grayscale, figsize=(8, 4), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, cumulative=compounded) - tpl = tpl.replace('{{vol_returns}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.yearly_returns(returns, benchmark, grayscale=grayscale, - figsize=(8, 4), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, compounded=compounded) - tpl = tpl.replace('{{eoy_returns}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.histogram(returns, grayscale=grayscale, - figsize=(8, 4), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, compounded=compounded) - tpl = tpl.replace('{{monthly_dist}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.daily_returns(returns, grayscale=grayscale, - figsize=(8, 3), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False) - tpl = tpl.replace('{{daily_returns}}', figfile.getvalue().decode()) + figfile = _get_utils()._file_stream() + _get_plots().returns( + returns, + benchmark, + match_volatility=True, + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compound=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{vol_returns}}", _embed_figure(figfile, figfmt)) + + # Yearly returns comparison chart + figfile = _get_utils()._file_stream() + _get_plots().yearly_returns( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{eoy_returns}}", _embed_figure(figfile, figfmt)) + + # Returns distribution histogram + figfile = _get_utils()._file_stream() + _get_plots().histogram( + returns, + benchmark, + grayscale=grayscale, + figsize=(7, 4), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{monthly_dist}}", _embed_figure(figfile, figfmt)) + + # Daily returns scatter plot + figfile = _get_utils()._file_stream() + _get_plots().daily_returns( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 3), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + prepare_returns=False, + active=active, + ) + tpl = tpl.replace("{{daily_returns}}", _embed_figure(figfile, figfmt)) + # Rolling beta analysis (only if benchmark exists) if benchmark is not None: - figfile = _utils._file_stream() - _plots.rolling_beta(returns, benchmark, grayscale=grayscale, - figsize=(8, 3), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False) - tpl = tpl.replace('{{rolling_beta}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.rolling_volatility(returns, benchmark, grayscale=grayscale, - figsize=(8, 3), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False) - tpl = tpl.replace('{{rolling_vol}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.rolling_sharpe(returns, grayscale=grayscale, - figsize=(8, 3), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False) - tpl = tpl.replace('{{rolling_sharpe}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.rolling_sortino(returns, grayscale=grayscale, - figsize=(8, 3), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False) - tpl = tpl.replace('{{rolling_sortino}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.drawdowns_periods(returns, grayscale=grayscale, - figsize=(8, 4), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, compounded=compounded) - tpl = tpl.replace('{{dd_periods}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.drawdown(returns, grayscale=grayscale, - figsize=(8, 3), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False) - tpl = tpl.replace('{{dd_plot}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.monthly_heatmap(returns, grayscale=grayscale, - figsize=(8, 4), cbar=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, compounded=compounded) - tpl = tpl.replace('{{monthly_heatmap}}', figfile.getvalue().decode()) - - figfile = _utils._file_stream() - _plots.distribution(returns, grayscale=grayscale, - figsize=(8, 4), subtitle=False, - savefig={'fname': figfile, 'format': 'svg'}, - show=False, ylabel=False, compounded=compounded) - tpl = tpl.replace('{{returns_dist}}', figfile.getvalue().decode()) - - tpl = _regex.sub(r'\{\{(.*?)\}\}', '', tpl) - tpl = tpl.replace('white-space:pre;', '') - + figfile = _get_utils()._file_stream() + _get_plots().rolling_beta( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 3), + subtitle=False, + window1=win_half_year, + window2=win_year, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + prepare_returns=False, + ) + tpl = tpl.replace("{{rolling_beta}}", _embed_figure(figfile, figfmt)) + + # Rolling volatility analysis + figfile = _get_utils()._file_stream() + _get_plots().rolling_volatility( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 3), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + period=win_half_year, + periods_per_year=win_year, + ) + tpl = tpl.replace("{{rolling_vol}}", _embed_figure(figfile, figfmt)) + + # Rolling Sharpe ratio analysis + figfile = _get_utils()._file_stream() + _get_plots().rolling_sharpe( + returns, + grayscale=grayscale, + figsize=(8, 3), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + period=win_half_year, + periods_per_year=win_year, + ) + tpl = tpl.replace("{{rolling_sharpe}}", _embed_figure(figfile, figfmt)) + + # Rolling Sortino ratio analysis + figfile = _get_utils()._file_stream() + _get_plots().rolling_sortino( + returns, + grayscale=grayscale, + figsize=(8, 3), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + period=win_half_year, + periods_per_year=win_year, + ) + tpl = tpl.replace("{{rolling_sortino}}", _embed_figure(figfile, figfmt)) + + # Drawdown periods analysis + figfile = _get_utils()._file_stream() + if isinstance(returns, _pd.Series): + _get_plots().drawdowns_periods( + returns, + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + title=returns.name, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{dd_periods}}", _embed_figure(figfile, figfmt)) + elif isinstance(returns, _pd.DataFrame): + # Handle multiple strategy columns + embed = [] + for col in returns.columns: + _get_plots().drawdowns_periods( + returns[col], + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + title=col, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + prepare_returns=False, + ) + embed.append(figfile) + tpl = tpl.replace("{{dd_periods}}", _embed_figure(embed, figfmt)) + + # Underwater (drawdown) plot + figfile = _get_utils()._file_stream() + _get_plots().drawdown( + returns, + grayscale=grayscale, + figsize=(8, 3), + subtitle=False, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + ) + tpl = tpl.replace("{{dd_plot}}", _embed_figure(figfile, figfmt)) + + # Monthly returns heatmap + figfile = _get_utils()._file_stream() + if isinstance(returns, _pd.Series): + _get_plots().monthly_heatmap( + returns, + benchmark, + grayscale=grayscale, + figsize=(8, 4), + cbar=False, + returns_label=returns.name, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + active=active, + ) + tpl = tpl.replace("{{monthly_heatmap}}", _embed_figure(figfile, figfmt)) + elif isinstance(returns, _pd.DataFrame): + # Handle multiple strategy columns + embed = [] + for col in returns.columns: + _get_plots().monthly_heatmap( + returns[col], + benchmark, + grayscale=grayscale, + figsize=(8, 4), + cbar=False, + returns_label=col, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + active=active, + ) + embed.append(figfile) + tpl = tpl.replace("{{monthly_heatmap}}", _embed_figure(embed, figfmt)) + + # Returns distribution analysis + figfile = _get_utils()._file_stream() + + if isinstance(returns, _pd.Series): + _get_plots().distribution( + returns, + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + title=returns.name, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + prepare_returns=False, + ) + tpl = tpl.replace("{{returns_dist}}", _embed_figure(figfile, figfmt)) + elif isinstance(returns, _pd.DataFrame): + # Handle multiple strategy columns + embed = [] + for col in returns.columns: + _get_plots().distribution( + returns[col], + grayscale=grayscale, + figsize=(8, 4), + subtitle=False, + title=col, + savefig={"fname": figfile, "format": figfmt}, + show=False, + ylabel="", + compounded=compounded, + prepare_returns=False, + ) + embed.append(figfile) + tpl = tpl.replace("{{returns_dist}}", _embed_figure(embed, figfmt)) + + # Clean up any remaining template placeholders + tpl = _regex.sub(r"\{\{(.*?)\}\}", "", tpl) + tpl = tpl.replace("white-space:pre;", "") + + # Handle output - either download in browser or save to file if output is None: - # _open_html(tpl) - _download_html(tpl, 'quantstats-tearsheet.html') + if _get_utils()._in_notebook(): + _download_html(tpl, download_filename) + else: + # Save to temp file and open in browser + with tempfile.NamedTemporaryFile( + mode="w", suffix=".html", delete=False, encoding="utf-8" + ) as f: + f.write(tpl) + temp_path = f.name + webbrowser.open("file://" + temp_path) return - with open(output, 'w', encoding='utf-8') as f: + # Write HTML content to specified output file + with open(output, "w", encoding="utf-8") as f: f.write(tpl) -def full(returns, benchmark=None, rf=0., grayscale=False, - figsize=(8, 5), display=True, compounded=True): - - dd = _stats.to_drawdown_series(returns) - dd_info = _stats.drawdown_details(dd).sort_values( - by='max drawdown', ascending=True)[:5] +def full( + returns, + benchmark=None, + rf=0.0, + grayscale=False, + figsize=(8, 5), + display=True, + compounded=True, + periods_per_year=252, + match_dates=True, + **kwargs, +): + """ + Generate a comprehensive performance analysis report. + + This function creates a full performance analysis including metrics, + worst drawdowns analysis, and complete visualization suite. It's designed + for detailed portfolio analysis and can handle both single strategies + and multiple strategy comparisons. + + Parameters + ---------- + returns : pd.Series or pd.DataFrame + Daily returns data for the strategy/portfolio + benchmark : pd.Series, str, or None, default None + Benchmark returns for comparison + rf : float, default 0.0 + Risk-free rate for calculations (as decimal) + grayscale : bool, default False + Whether to generate charts in grayscale + figsize : tuple, default (8, 5) + Figure size for plots as (width, height) + display : bool, default True + Whether to display results in notebook/console + compounded : bool, default True + Whether to compound returns for calculations + periods_per_year : int, default 252 + Number of trading periods per year + match_dates : bool, default True + Whether to align returns and benchmark start dates + **kwargs + Additional keyword arguments: + - strategy_title: Custom name for the strategy + - benchmark_title: Custom name for the benchmark + - active_returns: Whether to show active returns vs benchmark + + Returns + ------- + None + Displays comprehensive analysis including metrics, drawdowns, and plots + + Examples + -------- + >>> full(returns, benchmark='^GSPC', rf=0.02) + >>> full(returns, figsize=(10, 6), grayscale=True) + """ + # prepare timeseries + if match_dates: + returns = returns.dropna() + # Clean and prepare returns data + returns = _get_utils()._prepare_returns(returns) + + # Process benchmark if provided + if benchmark is not None: + benchmark = _get_utils()._prepare_benchmark(benchmark, returns.index, rf) + if match_dates is True: + returns, benchmark = _match_dates(returns, benchmark) - if not dd_info.empty: - dd_info.index = range(1, min(6, len(dd_info)+1)) - dd_info.columns = map(lambda x: str(x).title(), dd_info.columns) + # Extract title parameters from kwargs + benchmark_title = None + if benchmark is not None: + benchmark_title = kwargs.get("benchmark_title", "Benchmark") + strategy_title = kwargs.get("strategy_title", "Strategy") + active = kwargs.get("active_returns", False) - if _utils._in_notebook(): - iDisplay(iHTML(' +', ' ', obj)

- obj = _regex.sub(' + ', '', obj)

- obj = _regex.sub(' +', ' ', obj)

- obj = _regex.sub(' + ', '', obj)

+ """

+ Convert DataFrame to HTML table format for report generation.

+

+ This helper function converts pandas DataFrames to clean HTML table format

+ suitable for embedding in HTML reports. It removes default tabulate styling

+ and cleans up spacing for better presentation.

+

+ Parameters

+ ----------

+ obj : pd.DataFrame

+ DataFrame to convert to HTML table

+ showindex : str or bool, default "default"

+ Whether to show the DataFrame index in the HTML table.

+ "default" uses tabulate's default behavior

+

+ Returns

+ -------

+ str

+ HTML string containing the formatted table

+

+ Examples

+ --------

+ >>> html_str = _html_table(metrics_df)

+ >>> html_str = _html_table(metrics_df, showindex=False)

+ """

+ # Convert DataFrame to HTML table using tabulate

+ obj = _tabulate(

+ obj, headers="keys", tablefmt="html", floatfmt=".2f", showindex=showindex

+ )

+

+ # Remove default tabulate styling attributes

+ obj = obj.replace(' style="text-align: right;"', "")

+ obj = obj.replace(' style="text-align: left;"', "")

+ obj = obj.replace(' style="text-align: center;"', "")

+

+ # Clean up spacing in table cells

+ obj = _regex.sub(" +", " ", obj)

+ obj = _regex.sub(" + ", "", obj)

+ obj = _regex.sub(" +", " ", obj)

+ obj = _regex.sub(" + ", "", obj)

+

return obj

def _download_html(html, filename="quantstats-tearsheet.html"):

- jscode = _regex.sub(' +', ' ', """""".replace('\n', ''))

- jscode = jscode.replace('{{html}}', _regex.sub(

- ' +', ' ', html.replace('\n', '')))

- if _utils._in_notebook():

- iDisplay(iHTML(jscode.replace('{{filename}}', filename)))

+ a.click();""".replace(

+ "\n", ""

+ ),

+ )

+

+ # Insert HTML content and clean up formatting

+ jscode = jscode.replace("{{html}}", _regex.sub(" +", " ", html.replace("\n", "")))

+

+ # Execute JavaScript in notebook if in notebook environment

+ if _get_utils()._in_notebook():

+ iDisplay(iHTML(jscode.replace("{{filename}}", filename)))

def _open_html(html):

- jscode = _regex.sub(' +', ' ', """""".replace('\n', ''))

- jscode = jscode.replace('{{html}}', _regex.sub(

- ' +', ' ', html.replace('\n', '')))

- if _utils._in_notebook():

+ """.replace(

+ "\n", ""

+ ),

+ )

+

+ # Insert HTML content and clean up formatting

+ jscode = jscode.replace("{{html}}", _regex.sub(" +", " ", html.replace("\n", "")))

+

+ # Execute JavaScript in notebook if in notebook environment

+ if _get_utils()._in_notebook():

iDisplay(iHTML(jscode))

+

+

+def _embed_figure(figfiles, figfmt):

+ """

+ Embed matplotlib figures in HTML format for reports.

+

+ This helper function converts matplotlib figure objects to embedded

+ HTML format suitable for inclusion in HTML reports. It handles both

+ SVG and base64-encoded image formats.

+

+ Parameters

+ ----------

+ figfiles : io.StringIO or list of io.StringIO

+ File-like objects containing figure data. Can be single figure

+ or list of figures for multiple plots

+ figfmt : str

+ Format for the figures ('svg', 'png', 'jpg', etc.)

+

+ Returns

+ -------

+ str

+ HTML string with embedded figure(s) ready for inclusion in report

+

+ Examples

+ --------

+ >>> embed_str = _embed_figure(figfile, 'svg')

+ >>> embed_str = _embed_figure([fig1, fig2], 'png')

+ """

+ # Handle multiple figures

+ if isinstance(figfiles, list):

+ embed_string = "\n"

+ for figfile in figfiles:

+ figbytes = figfile.getvalue()

+ if figfmt == "svg":

+ # SVG can be embedded directly as text

+ return figbytes.decode()

+ # For other formats, encode as base64 data URI

+ data_uri = _b64encode(figbytes).decode()

+ embed_string.join(

+ ' '.format(figfmt, data_uri)

+ )

+ else:

+ # Handle single figure

+ figbytes = figfiles.getvalue()

+ if figfmt == "svg":

+ # SVG can be embedded directly as text

+ return figbytes.decode()

+ # For other formats, encode as base64 data URI

+ data_uri = _b64encode(figbytes).decode()

+ embed_string = ''.format(figfmt, data_uri)

+

+ return embed_string

diff --git a/quantstats/stats.py b/quantstats/stats.py

index 2c348760..5a0c6e36 100644

--- a/quantstats/stats.py

+++ b/quantstats/stats.py

@@ -1,10 +1,9 @@

#!/usr/bin/env python

-# -*- coding: UTF-8 -*-

#

# QuantStats: Portfolio analytics for quants

# https://github.com/ranaroussi/quantstats

#

-# Copyright 2019 Ran Aroussi

+# Copyright 2019-2025 Ran Aroussi

#

# Licensed under the Apache License, Version 2.0 (the "License");

# you may not use this file except in compliance with the License.

@@ -18,699 +17,3295 @@

# See the License for the specific language governing permissions and

# limitations under the License.

+"""

+Portfolio Statistics Module

+

+This module provides comprehensive statistical analysis functions for portfolio

+performance evaluation, risk assessment, and benchmarking. It includes functions

+for calculating various return metrics, risk ratios, drawdown analysis, and

+comparison with benchmarks.

+

+The module is designed to work with pandas Series and DataFrames containing

+return data, price data, or performance metrics.

+"""

+

+from warnings import warn

+from typing import Literal

import pandas as _pd

import numpy as _np

-from math import ceil as _ceil

-from scipy.stats import (

- norm as _norm, linregress as _linregress

-)

+from numpy.typing import NDArray

+from math import ceil as _ceil, sqrt as _sqrt

+from scipy.stats import norm as _norm, linregress as _linregress

from . import utils as _utils

+from ._compat import safe_concat

+from .utils import validate_input

+# Type aliases for common types (Python 3.10+ syntax)

+Returns = _pd.Series | _pd.DataFrame

+"""Type alias for returns data: can be a pandas Series or DataFrame."""

# ======== STATS ========

-def pct_rank(prices, window=60):

- """ rank prices by window """

+

+def pct_rank(prices: _pd.Series, window: int = 60) -> _pd.Series:

+ """

+ Calculate the percentile rank of prices over a rolling window.

+

+ This function computes the percentile rank (0-100) of each price point

+ within a rolling window, useful for identifying relative position of

+ current prices compared to recent history.

+

+ Args:

+ prices (pd.Series): Series of price data

+ window (int): Rolling window size for rank calculation (default: 60)

+

+ Returns:

+ pd.Series: Percentile ranks (0-100 scale)

+

+ Example:

+ >>> prices = pd.Series([100, 105, 110, 95, 120])

+ >>> ranks = pct_rank(prices, window=3)

+ >>> print(ranks)

+ """

+ # Create rolling window shifts and transpose for ranking

rank = _utils.multi_shift(prices, window).T.rank(pct=True).T

- return rank.iloc[:, 0] * 100.

+ # Extract first column and convert to percentage scale

+ return rank.iloc[:, 0] * 100.0

-def compsum(returns):

- """ Calculates rolling compounded returns """

- return returns.add(1).cumprod() - 1

+def compsum(returns: Returns) -> Returns:

+ """

+ Calculate rolling compounded returns (cumulative product).

+ This function computes the cumulative compounded returns by adding 1

+ to each return, taking the cumulative product, and subtracting 1.

-def comp(returns):

- """ Calculates total compounded returns """

- return returns.add(1).prod() - 1

+ Args:

+ returns: Series or DataFrame of returns

+ Returns:

+ Cumulative compounded returns (same type as input)

-def expected_return(returns, aggregate=None, compounded=True):

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, -0.01, 0.03])

+ >>> cumulative = compsum(returns)

+ >>> print(cumulative)

"""

- returns the expected return for a given period

- by calculating the geometric holding period return

+ # Add 1 to convert returns to growth factors, then cumulative product

+ return returns.add(1).cumprod(axis=0) - 1

+

+

+def comp(returns: Returns) -> _pd.Series | float:

"""

- returns = _utils._prepare_returns(returns)

+ Calculate total compounded returns (final cumulative return).

+

+ This function computes the total compounded return over the entire period

+ by converting returns to growth factors and taking their product.

+

+ Args:

+ returns (pd.Series): Series of returns

+

+ Returns:

+ float: Total compounded return

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, -0.01, 0.03])

+ >>> total_return = comp(returns)

+ >>> print(total_return)

+ """

+ # Convert returns to growth factors, take product, subtract 1

+ return returns.add(1).prod(axis=0) - 1

+

+

+def distribution(

+ returns: Returns,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> dict:

+ """

+ Analyze return distributions across different time periods.

+

+ This function calculates return distributions (including outliers) for

+ daily, weekly, monthly, quarterly, and yearly periods. It identifies

+ outliers using the IQR method (1.5 * IQR beyond Q1/Q3).

+

+ Args:

+ returns (pd.Series): Return series to analyze

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ dict: Dictionary containing distribution data for each period

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, -0.01],

+ ... index=pd.date_range('2023-01-01', periods=3))

+ >>> dist = distribution(returns)

+ >>> print(dist['Daily']['values'])

+ """

+ def get_outliers(data):

+ """

+ Identify outliers using the IQR method.

+

+ Uses 1.5 * IQR rule: values beyond Q1 - 1.5*IQR or Q3 + 1.5*IQR

+ are considered outliers.

+ """

+ # https://datascience.stackexchange.com/a/57199

+ Q1 = data.quantile(0.25) # First quartile

+ Q3 = data.quantile(0.75) # Third quartile

+ IQR = Q3 - Q1 # Interquartile range

+

+ # Create filter for non-outlier values

+ filtered = (data >= Q1 - 1.5 * IQR) & (data <= Q3 + 1.5 * IQR)

+

+ return {

+ "values": data.loc[filtered].tolist(),

+ "outliers": data.loc[~filtered].tolist(),

+ }

+

+ # Handle DataFrame input by selecting appropriate column

+ if isinstance(returns, _pd.DataFrame):

+ warn(

+ "Pandas DataFrame was passed (Series expected). "

+ "Only first column will be used."

+ )

+ returns = returns.copy()

+ returns.columns = map(str.lower, returns.columns)

+ if len(returns.columns) > 1 and "close" in returns.columns:

+ returns = returns["close"]

+ else:

+ returns = returns[returns.columns[0]]

+

+ # Choose aggregation function based on compounded parameter

+ apply_fnc = comp if compounded else _np.sum

+ daily = returns.dropna()

+

+ # Prepare returns if requested

+ if prepare_returns:

+ daily = _utils._prepare_returns(daily)

+

+ # Calculate distributions for different time periods

+ return {

+ "Daily": get_outliers(daily),

+ "Weekly": get_outliers(daily.resample("W-MON").apply(apply_fnc)),

+ "Monthly": get_outliers(daily.resample("ME").apply(apply_fnc)),

+ "Quarterly": get_outliers(daily.resample("QE").apply(apply_fnc)),

+ "Yearly": get_outliers(daily.resample("YE").apply(apply_fnc)),

+ }

+

+

+def expected_return(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> float:

+ """

+ Calculate the expected return (geometric mean) for a given period.

+

+ This function computes the geometric holding period return, which represents

+ the expected return per period based on historical data. It's calculated

+ as the nth root of the product of (1 + returns) minus 1.

+

+ Args:

+ returns (pd.Series): Return series

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ float: Expected return per period

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, -0.01, 0.03])

+ >>> expected = expected_return(returns)

+ >>> print(f"Expected return: {expected:.4f}")

+ """

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns if period specified

returns = _utils.aggregate_returns(returns, aggregate, compounded)

- return _np.product(1 + returns) ** (1 / len(returns)) - 1

+ # Calculate geometric mean: (product of (1 + returns))^(1/n) - 1

+ return _np.prod(1 + returns, axis=0) ** (1 / len(returns)) - 1

+

+

+def geometric_mean(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+) -> float:

+ """

+ Calculate geometric mean of returns.

+

+ This is a shorthand function for expected_return() with the same parameters.

+

+ Args:

+ returns (pd.Series): Return series

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+

+ Returns:

+ float: Geometric mean of returns

+ """

+ return expected_return(returns, aggregate, compounded)

+

+

+def ghpr(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+) -> float:

+ """

+ Calculate Geometric Holding Period Return.

+

+ This is a shorthand function for expected_return() with the same parameters.

+ GHPR represents the average rate of return per period.

+

+ Args:

+ returns (pd.Series): Return series

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+

+ Returns:

+ float: Geometric holding period return

+ """

+ return expected_return(returns, aggregate, compounded)

+

+

+def outliers(returns: Returns, quantile: float = 0.95) -> Returns:

+ """

+ Identify and return outlier returns above a specified quantile.

+

+ This function filters returns to show only those above the specified

+ quantile threshold, helping identify extreme positive performance periods.

-def geometric_mean(retruns, aggregate=None, compounded=True):

- """ shorthand for expected_return() """

- return expected_return(retruns, aggregate, compounded)

+ Args:

+ returns (pd.Series): Return series to analyze

+ quantile (float): Quantile threshold (default: 0.95 for 95th percentile)

+

+ Returns:

+ pd.Series: Returns above the quantile threshold

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, 0.05, -0.01, 0.10])

+ >>> outlier_returns = outliers(returns, quantile=0.90)

+ >>> print(outlier_returns)

+ """

+ # Filter returns above the specified quantile and remove NaN values

+ return returns[returns > returns.quantile(quantile)].dropna(how="all")

-def ghpr(retruns, aggregate=None, compounded=True):

- """ shorthand for expected_return() """

- return expected_return(retruns, aggregate, compounded)

+def remove_outliers(returns: Returns, quantile: float = 0.95) -> Returns:

+ """

+ Remove outlier returns above a specified quantile.

+ This function filters out extreme returns above the quantile threshold,

+ useful for robust statistical analysis by removing extreme values.

-def outliers(returns, quantile=.95):

- """returns series of outliers """

- return returns[returns > returns.quantile(quantile)].dropna(how='all')

+ Args:

+ returns (pd.Series): Return series to filter

+ quantile (float): Quantile threshold (default: 0.95 for 95th percentile)

+ Returns:

+ pd.Series: Returns below the quantile threshold

-def remove_outliers(returns, quantile=.95):

- """ returns series of returns without the outliers """

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, 0.05, -0.01, 0.10])

+ >>> filtered = remove_outliers(returns, quantile=0.90)

+ >>> print(filtered)

+ """

+ # Keep only returns below the specified quantile threshold

return returns[returns < returns.quantile(quantile)]

-def best(returns, aggregate=None, compounded=True):

- """ returns the best day/month/week/quarter/year's return """

- returns = _utils._prepare_returns(returns)

+def best(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> float:

+ """

+ Find the best (highest) return for a given period.

+

+ This function identifies the maximum return over the specified aggregation

+ period, helping identify the best performing period in the dataset.

+

+ Args:

+ returns (pd.Series): Return series to analyze

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ float: Best (maximum) return for the period

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, -0.01, 0.03])

+ >>> best_return = best(returns)

+ >>> print(f"Best return: {best_return:.4f}")

+ """

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns and find maximum

return _utils.aggregate_returns(returns, aggregate, compounded).max()

-def worst(returns, aggregate=None, compounded=True):

- """ returns the worst day/month/week/quarter/year's return """

- returns = _utils._prepare_returns(returns)

+def worst(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> float:

+ """

+ Find the worst (lowest) return for a given period.

+

+ This function identifies the minimum return over the specified aggregation

+ period, helping identify the worst performing period in the dataset.

+

+ Args:

+ returns (pd.Series): Return series to analyze

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ float: Worst (minimum) return for the period

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, -0.01, 0.03])

+ >>> worst_return = worst(returns)

+ >>> print(f"Worst return: {worst_return:.4f}")

+ """

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns and find minimum

return _utils.aggregate_returns(returns, aggregate, compounded).min()

-def consecutive_wins(returns, aggregate=None, compounded=True):

- """ returns the maximum consecutive wins by day/month/week/quarter/year """

- returns = _utils._prepare_returns(returns)

+def consecutive_wins(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> int:

+ """

+ Calculate the maximum number of consecutive winning periods.

+

+ This function identifies the longest streak of positive returns, which

+ helps assess the consistency of positive performance.

+

+ Args:

+ returns (pd.Series): Return series to analyze

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ int: Maximum number of consecutive winning periods

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.02, 0.03, -0.01, 0.02])

+ >>> max_wins = consecutive_wins(returns)

+ >>> print(f"Max consecutive wins: {max_wins}")

+ """

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns and convert to boolean (positive = True)

returns = _utils.aggregate_returns(returns, aggregate, compounded) > 0

- return _utils.count_consecutive(returns).max()

+ # Count consecutive True values and return maximum

+ return _utils._count_consecutive(returns).max()

-def consecutive_losses(returns, aggregate=None, compounded=True):

+

+def consecutive_losses(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> int:

"""

- returns the maximum consecutive losses by

- day/month/week/quarter/year

+ Calculate the maximum number of consecutive losing periods.

+

+ This function identifies the longest streak of negative returns, which

+ helps assess the potential for extended drawdown periods.

+

+ Args:

+ returns (pd.Series): Return series to analyze

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ int: Maximum number of consecutive losing periods

+

+ Example:

+ >>> returns = pd.Series([0.01, -0.02, -0.01, -0.01, 0.02])

+ >>> max_losses = consecutive_losses(returns)

+ >>> print(f"Max consecutive losses: {max_losses}")

"""

- returns = _utils._prepare_returns(returns)

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns and convert to boolean (negative = True)

returns = _utils.aggregate_returns(returns, aggregate, compounded) < 0

- return _utils.count_consecutive(returns).max()

+ # Count consecutive True values and return maximum

+ return _utils._count_consecutive(returns).max()

-def exposure(returns):

- """ returns the market exposure time (returns != 0) """

- returns = _utils._prepare_returns(returns)

+

+def exposure(

+ returns: Returns,

+ prepare_returns: bool = True,

+) -> float | _pd.Series:

+ """

+ Calculate market exposure time as percentage of periods with non-zero returns.

+

+ This function measures how often the strategy was actually invested

+ (had non-zero returns) versus being in cash or having zero positions.

+

+ Args:

+ returns (pd.Series or pd.DataFrame): Return series or DataFrame

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ float or pd.Series: Exposure percentage (0-1 scale)

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.00, 0.02, 0.00, 0.03])

+ >>> exp = exposure(returns)

+ >>> print(f"Market exposure: {exp:.2%}")

+ """

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

def _exposure(ret):

+ """

+ Calculate exposure for a single return series.

+

+ Counts non-NaN, non-zero returns and divides by total periods.

+ Rounds up to nearest percent to avoid zero exposure from rounding.

+ """

+ # Count non-NaN and non-zero returns

ex = len(ret[(~_np.isnan(ret)) & (ret != 0)]) / len(ret)

+ # Round up to nearest percent

return _ceil(ex * 100) / 100

+ # Handle DataFrame input by calculating exposure for each column

if isinstance(returns, _pd.DataFrame):

_df = {}

for col in returns.columns:

_df[col] = _exposure(returns[col])

return _pd.Series(_df)

+

return _exposure(returns)

-def win_rate(returns, aggregate=None, compounded=True):

- """ calculates the win ratio for a period """

+def win_rate(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> float | _pd.Series:

+ """

+ Calculate the win rate (percentage of profitable periods).

+

+ This function computes the ratio of positive returns to total non-zero

+ returns, providing a measure of how often the strategy generates profits.

+

+ Args:

+ returns (pd.Series or pd.DataFrame): Return series or DataFrame

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ float or pd.Series: Win rate as decimal (0-1 scale)

+

+ Example:

+ >>> returns = pd.Series([0.01, -0.02, 0.03, -0.01, 0.02])

+ >>> wr = win_rate(returns)

+ >>> print(f"Win rate: {wr:.2%}")

+ """

def _win_rate(series):

- try:

- return len(series[series > 0]) / len(series[series != 0])

- except Exception:

- return 0.

+ """

+ Calculate win rate for a single return series.

- returns = _utils._prepare_returns(returns)

+ Handles edge cases like no non-zero returns and provides

+ error handling for calculation issues.

+ """

+ try:

+ # Filter out zero returns (periods with no trading)

+ non_zero_returns = series[series != 0]

+ if len(non_zero_returns) == 0:

+ warn("No non-zero returns found for win rate calculation, returning 0.0")

+ return 0.0

+

+ # Calculate ratio of positive returns to non-zero returns

+ return len(series[series > 0]) / len(non_zero_returns)

+ except (ValueError, TypeError) as e:

+ warn(f"Error calculating win rate: {e}, returning 0.0")

+ return 0.0

+

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns if period specified

if aggregate:

returns = _utils.aggregate_returns(returns, aggregate, compounded)

+ # Handle DataFrame input by calculating win rate for each column

if isinstance(returns, _pd.DataFrame):

_df = {}

for col in returns.columns:

_df[col] = _win_rate(returns[col])

-

return _pd.Series(_df)

return _win_rate(returns)

-def avg_return(returns, aggregate=None, compounded=True):

+def avg_return(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> float:

"""

- calculates the average return/trade return for a period

- returns = _utils._prepare_returns(returns)

+ Calculate the average return per period (excluding zero returns).

+

+ This function computes the mean of non-zero returns, providing insight

+ into the typical magnitude of returns when the strategy is active.

+

+ Args:

+ returns (pd.Series): Return series to analyze

+ aggregate (str): Aggregation period ('D', 'W', 'M', 'Q', 'Y')

+ compounded (bool): Whether to compound returns (default: True)

+ prepare_returns (bool): Whether to prepare returns first (default: True)

+

+ Returns:

+ float: Average return per period

+

+ Example:

+ >>> returns = pd.Series([0.01, 0.00, 0.02, -0.01, 0.03])

+ >>> avg_ret = avg_return(returns)

+ >>> print(f"Average return: {avg_ret:.4f}")

"""

- returns = _utils._prepare_returns(returns)

+ if prepare_returns:

+ returns = _utils._prepare_returns(returns)

+

+ # Aggregate returns if period specified

if aggregate:

returns = _utils.aggregate_returns(returns, aggregate, compounded)

+

+ # Calculate mean of non-zero returns

return returns[returns != 0].dropna().mean()

-def avg_win(returns, aggregate=None, compounded=True):

+def avg_win(

+ returns: Returns,

+ aggregate: str | None = None,

+ compounded: bool = True,

+ prepare_returns: bool = True,

+) -> float:

"""

- calculates the average winning

- return/trade return for a period

+ Calculate the average winning return (mean of positive returns).

+

+ This function computes the mean of positive returns only, showing

+ the typical magnitude of profitable periods.

+

+ Args: